Understanding the Distinctions Between Chapter 7 and Chapter 13 Bankruptcy

Learn the key differences between Chapter 7 and Chapter 13 bankruptcy, including how each works, eligibility requirements, and which option may be right for your financial situation. A clear, user-friendly guide to help you understand your bankruptcy choices and make informed decisions.

Robert Durham

3/1/20262 min read

Introduction

Bankruptcy can often feel overwhelming, yet it serves as an essential legal mechanism for individuals facing financial distress. Among the various types of bankruptcy, Chapter 7 and Chapter 13 are the most commonly pursued by individuals. Understanding the differences between these two chapters is crucial in determining which is the best option based on individual circumstances.

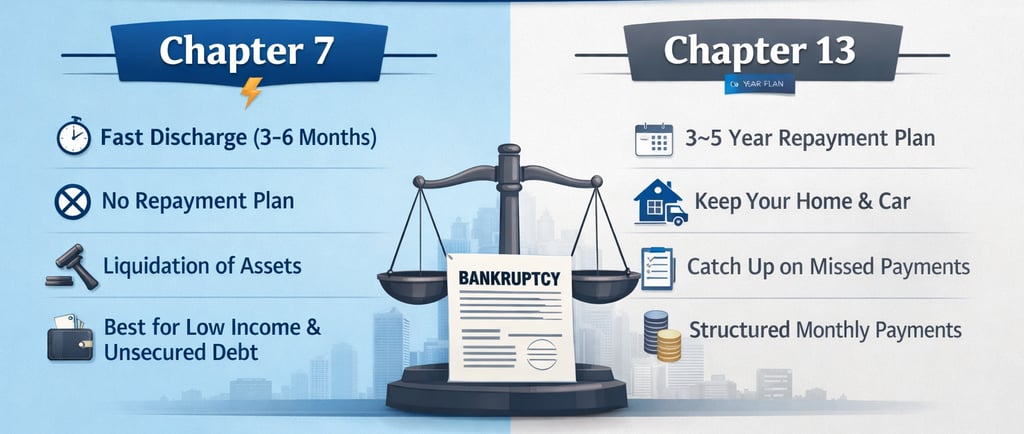

Chapter 7 Bankruptcy Explained

Chapter 7 bankruptcy, often referred to as liquidation bankruptcy, is designed to eliminate unsecured debts. This includes credit card debt, medical bills, and personal loans, allowing individuals to make a fresh financial start. Under this chapter, a bankruptcy trustee is appointed to evaluate the debtor's assets. Non-exempt assets may be sold to repay creditors, while exempt assets are retained by the debtor.

One significant advantage of Chapter 7 is the swift nature of the process. Typically, the entire bankruptcy process can be completed within three to six months. However, it is important to note that Chapter 7 has strict eligibility requirements based on income and asset criteria. If an individual's income exceeds the state median, they may not qualify for this type of bankruptcy.

Chapter 13 Bankruptcy Overview

In contrast, Chapter 13 bankruptcy is designed for individuals with a regular income who wish to develop a repayment plan for their debts. This chapter allows individuals to retain their assets while repaying creditors over a specified period, typically three to five years. The repayment plan is formulated according to the debtor's income, allowing them to manage their debts more feasibly.

One of the primary benefits of Chapter 13 is the protection it offers against foreclosure. Debtors can save their homes from foreclosure proceeding by keeping up with their proposed repayment plan. Moreover, Chapter 13 may also allow for the potential reduction of secured debts, making it a favorable option for many individuals.

Key Differences and Considerations

The fundamental difference between Chapter 7 and Chapter 13 bankruptcy lies in the approach to debt resolution. Chapter 7 focuses on debt discharge through asset liquidation, while Chapter 13 emphasizes debt repayment through a structured plan. Individuals considering these options must evaluate their income, assets, and long-term financial goals.

Ultimately, choosing between Chapter 7 and Chapter 13 bankruptcy involves careful consideration. It is essential to consult with a financial advisor or bankruptcy attorney to understand the implications and ensure that the chosen path aligns with one’s financial recovery goals. Bankruptcy may serve as a viable solution to severe financial challenges when approached with detailed understanding and planning.

Newsletter

Copyright © 2026

Robert Vance Durham Jr.

All rights reserved.

No part of this book may be reproduced, distributed, or transmitted in any form or by any means—electronic or mechanical—without prior written permission of the author, except for brief quotations used in reviews.